t location-scale model

For many financial data, it turns out the historical logreturns often can not be approximated well by a normal distribution. In fact, the heavy-tails effect and the higher density near the mean can not be caputred by $N(\mu,\sigma)$.

Luckily, we can use t location-scale model to capture all these missing characteristics. Before we jump into the defintion and application of this model, we have to revisit the student-t distribution.

student’s t-distribution

We can define student-t distribution through two approach.

Student’s t-distribution has the probability density function given by:

\[f(t)=\frac{\Gamma\left(\frac{\nu+1}{2}\right)}{\sqrt{\nu \pi} \Gamma\left(\frac{\nu}{2}\right)}\left(1+\frac{t^{2}}{\nu}\right)^{-\frac{\nu+1}{2}}\]where $\nu $ is the number of degrees of freedom and $\Gamma$ is the gamma function.

Statistics

When $0<dof<=1$, all moments are undefined.

The theoretical statistics (i.e., in the absence of sampling error) when $dof>1$ are as follows.

- Mean=Mode=Median=0

- \[Variance = \begin{cases} \infty, & \text{if $v\leq$ 2} \\ \frac{v}{v-2}, & \text{if $v>$ 2} \end{cases}\]

- Skewness=0 if v>3

- \[Kurtosiso = \begin{cases} \infty, & \text{if $2<v\leq4$ } \\ 3+\frac{6}{v-4}, & \text{if $v>4$} \end{cases}\]

t Location-Scale Distribution

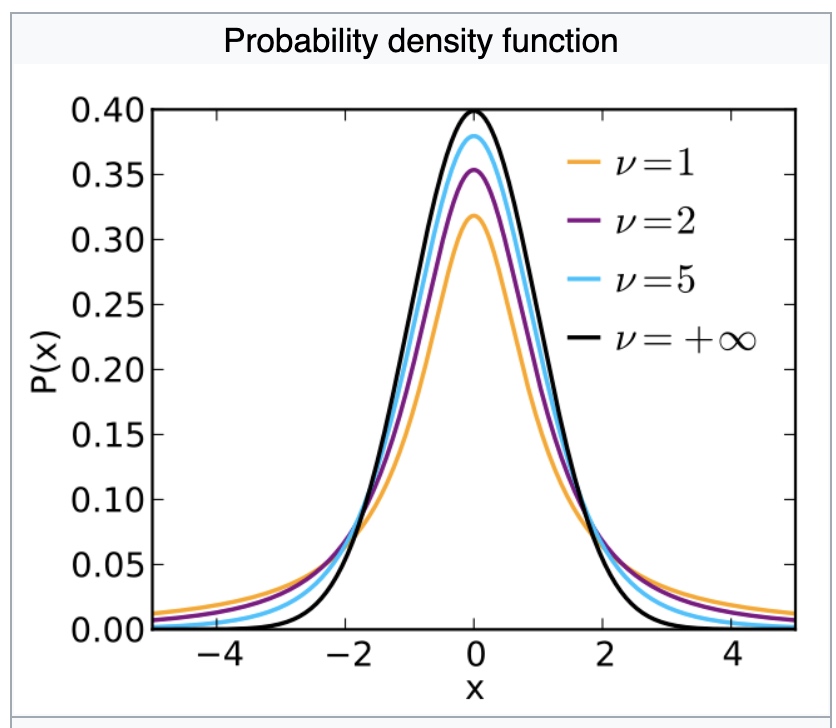

The t location-scale distribution is useful for modeling data distributions with heavier tails (more prone to outliers) than the normal distribution. It approaches the normal distribution as ν approaches infinity, and smaller values of ν yield heavier tails.

A t Location-Scale Distributed random variable has 3 parameters $(\mu,\sigma,\nu)$, and can be defined as:

\[r=\mu + \sigma* T(\nu)\]If we set

\[\sigma =\sqrt{\frac{v-2}{v}}\]r will have a variance of 1, and now it is called as a rescaled t-distribution

Here is how the rescaled t-distribution changes as the degree of freedom increases.

As we can see, when $nu$ is smaller:

- near the mean: the probability density function will be higher than “normal”

- the left and right tails: the PDF will also be higher than “normal”, which means fat tails

Codes in Python

histogram visualization

Draw the histogram and the PDF for fitted t location-scale and normal distribution.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

def myhist(df_input, bins=30):

import matplotlib.pyplot as plt

import matplotlib.style as style

import scipy.stats as stats

import numpy as np

df_input = np.array(df_input)

if df_input.ndim > 1:

if df_input.shape[0] > 1:

df_input = df_input[:, 0]

else:

df_input = df_input[0, :]

style.use("ggplot")

plt.rcParams["figure.figsize"] = (6, 4)

plt.figure(dpi=100)

heightofbins, aa, bb = plt.hist(df_input, bins)

mu = df_input.mean()

std = df_input.std()

lowb = df_input.min()

upb = df_input.max()

# can use stats.norm.fit to get the std, mu

# nloc,nscale=stats.norm.fit(df_input)

# fit the data with a t location-scale model with MLE

## r=loc + scale * T(dof)

tdof, tloc, tscale = stats.t.fit(df_input)

# Change the shape of PDF to match the hist

## both norm and t distribution pdf are multiplied by a same number

### norm distribution

xx = stats.norm.pdf(np.linspace(lowb - std, upb + std, 1000), loc=mu, scale=std)

xx = xx * np.max(heightofbins) / stats.t.pdf(mu, df=tdof, loc=tloc, scale=tscale)

plt.plot(np.linspace(lowb - std, upb + std, 1000), xx)

### rescaled t distribution

y = stats.t.pdf(

np.linspace(lowb - std, upb + std, 1000), df=tdof, loc=tloc, scale=tscale

)

y = y * np.max(heightofbins) / stats.t.pdf(mu, df=tdof, loc=tloc, scale=tscale)

plt.plot(np.linspace(lowb - std, upb + std, 1000), y)

plt.legend(["Normal PDF", "Rescaled t Distribution", "Sample Distribution"])

### plot the sample kurtosis and skewness

kur = stats.kurtosis(df_input)

skew = stats.skew(df_input)

x = mu + std

y = 0.5 * np.max(heightofbins)

plt.text(x, y, "Skewness:{:.2f},Kurtosis:{:.2f}".format(skew, kur))

plt.show()

Value at risk

The following function can calculate the Var_001, Var_005 for given data. It has 3 different methods to derive the vars:

- norm

- t

- historical

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

def myvar(df_input, alphas=[0.01, 0.05], method="all", tell=True):

if method not in ["all", "norm", "t", "historical"]:

print("Fail: wrong method! Please use one of the following method:")

for i in ["all", "norm", "t", "historical"]:

print(i)

return "Error"

import matplotlib.pyplot as plt

import matplotlib.style as style

import scipy.stats as stats

import numpy as np

alphas = np.array(alphas)

try:

palphas = [item * 100 for item in alphas]

except:

palphas = 100 * alphas

df_input = np.array(df_input)

if df_input.ndim > 1:

if df_input.shape[0] > 1:

df_input = df_input[:, 0]

else:

df_input = df_input[0, :]

# parametric method with norm distribution

# Analytic Approach

if method == "norm" or method == "all":

nloc, nscale = stats.norm.fit(df_input)

vars = stats.norm.ppf(alphas, loc=nloc, scale=nscale)

if tell == True or method == "all":

print("Use Norm-Distribution model:")

try:

for var, alpha in zip(vars, alphas):

print("Var {}: \t{} ".format(alpha, var))

except:

for var, alpha in zip([vars], [alphas]):

print("Var {}: \t{} ".format(alpha, var))

if method != "all":

return vars

# parametric method with t location-scale distribution

# fit the data with a t location-scale model with MLE

## r=loc + scale * T(dof)

if method == "t" or method == "all":

tdof, tloc, tscale = stats.t.fit(df_input)

vars = stats.t.ppf(alphas, df=tdof, loc=tloc, scale=tscale)

if tell == True or method == "all":

print("Use t location-scale model:")

try:

for var, alpha in zip(vars, alphas):

print("Var {}: \t{} ".format(alpha, var))

except:

for var, alpha in zip([vars], [alphas]):

print("Var {}: \t{} ".format(alpha, var))

if method != "all":

return vars

# historical method

if method == "historical" or method == "all":

vars = np.percentile(df_input, palphas)

if tell == True or method == "all":

print("Use Historical Approach:")

try:

for var, alpha in zip(vars, alphas):

print("Var {}: \t{} ".format(alpha, var))

except:

for var, alpha in zip([vars], [alphas]):

print("Var {}: \t{} ".format(alpha, var))

if method != "all":

return vars

if __name__ == "__main__":

print("This is my Var module")

import scipy.stats as stats

df = stats.t.rvs(df=5, scale=2, size=10000, loc=0)

myvar(df,alphas=[0.01,0.05,0.1])

xx = stats.t.ppf(df=5, scale=2, loc=0, q=[0.01, 0.05, 0.1])

print("Real Vars:")

print(xx)

Espected Shortfall

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

def myes(df_input, alphas=[0.01, 0.05], num_of_simus=1000000, method="all", tell=True):

if method not in ["all", "norm", "t", "historical"]:

print("Fail: wrong method! Please use one of the following method:")

for i in ["all", "norm", "t", "historical"]:

print(i)

return "Error"

import matplotlib.pyplot as plt

import matplotlib.style as style

import scipy.stats as stats

import numpy as np

alphas = np.array(alphas)

try:

palphas = [item * 100 for item in alphas]

except:

palphas = 100 * alphas

df_input = np.array(df_input)

if df_input.ndim > 1:

if df_input.shape[0] > 1:

df_input = df_input[:, 0]

else:

df_input = df_input[0, :]

# parametric method with norm distribution

if method == "norm" or method == "all":

nloc, nscale = stats.norm.fit(df_input)

vars = stats.norm.ppf(alphas, loc=nloc, scale=nscale)

nrvs = stats.norm.rvs(loc=nloc, scale=nscale, size=num_of_simus)

try:

ess = [nrvs[nrvs < var].mean() for var in vars]

except:

ess = nrvs[nrvs < vars].mean()

if tell == True or method == "all":

print("Use Analytical Norm-Distribution model:")

try:

for es, alpha in zip(ess, alphas):

print("ES {}: \t{} ".format(alpha, es))

except:

for es, alpha in zip([ess], [alphas]):

print("ES {}: \t{} ".format(alpha, es))

if method != "all":

return ess

# parametric method with t location-scale distribution

# fit the data with a t location-scale model with MLE

## r=loc + scale * T(dof)

if method == "t" or method == "all":

tdof, tloc, tscale = stats.t.fit(df_input)

vars = stats.t.ppf(alphas, df=tdof, loc=tloc, scale=tscale)

trvs = stats.t.rvs(df=tdof, scale=tscale, size=num_of_simus, loc=tloc)

try:

ess = [nrvs[nrvs < var].mean() for var in vars]

except:

ess = nrvs[nrvs < vars].mean()

if tell == True or method == "all":

print("Use Analytical t location-scale model:")

try:

for es, alpha in zip(ess, alphas):

print("ES {}: \t{} ".format(alpha, es))

except:

for es, alpha in zip([ess], [alphas]):

print("ES {}: \t{} ".format(alpha, es))

if method != "all":

return ess

# historical method

if method == "historical" or method == "all":

vars = np.percentile(df_input, palphas)

try:

ess = [nrvs[nrvs < var].mean() for var in vars]

except:

ess = nrvs[nrvs < vars].mean()

if tell == True or method == "all":

print("Use Historical Approach:")

try:

for es, alpha in zip(ess, alphas):

print("ES {}: \t{} ".format(alpha, es))

except:

for es, alpha in zip([ess], [alphas]):

print("ES {}: \t{} ".format(alpha, es))

if method != "all":

return ess

if __name__ == "__main__":

print("This is my Expected Shortfall module")

import scipy.stats as stats

# for calculating ES, we only have 1% or 5% useful data, therefore we want to increase the number of simulations

df = stats.t.rvs(df=5, scale=2, size=10000, loc=0)

myes(df, num_of_simus=10000000, alphas=[0.01, 0.05, 0.1])

Application

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

if __name__ == "__main__":

print("This is my first module")

from WindPy import w

import scipy.stats as stats

w.start() # 默认命令超时时间为120秒,如需设置超时时间可以加入waitTime参数,例如waitTime=60,即设置命令超时时间为60秒

print("WindPy是否已经登录成功:{}".format(w.isconnected())) # 判断WindPy是否已经登录成功

eroc, df = w.wsd("USDCNY.EX", "close", "2010-01-01",

"2020-12-28", usedf=True)

myhist(df.diff().dropna(), bins=100)

myvar(df.diff().dropna(), method="t", tell=True)

import pandas as pd

df.index = pd.to_datetime(df.index)

for i in range(2015, 2021):

print("For year {}:".format(i))

[var1, var2] = myvar(

-df[df.index.year == i].diff().dropna(), method="t", tell=False

)

print("Var_001={:.5f}, Var_005={:.5f}".format(var1, var2))

parameters = stats.t.fit(-df[df.index.year == i].diff().dropna())

print("DF={}\t Loc={}\t Scale={}".format(*parameters))

print("The stats are:")

statistics = stats.t.stats(*parameters, moments="mvsk")

print("Mean={}\t Variance={}\t Skew={}\t Kurtosis={}".format(*statistics))

print("-------------------------------------------")

Comments